How dynamic asset allocation boost risk-adjusted performance

Democratizing institutional investment insights and services

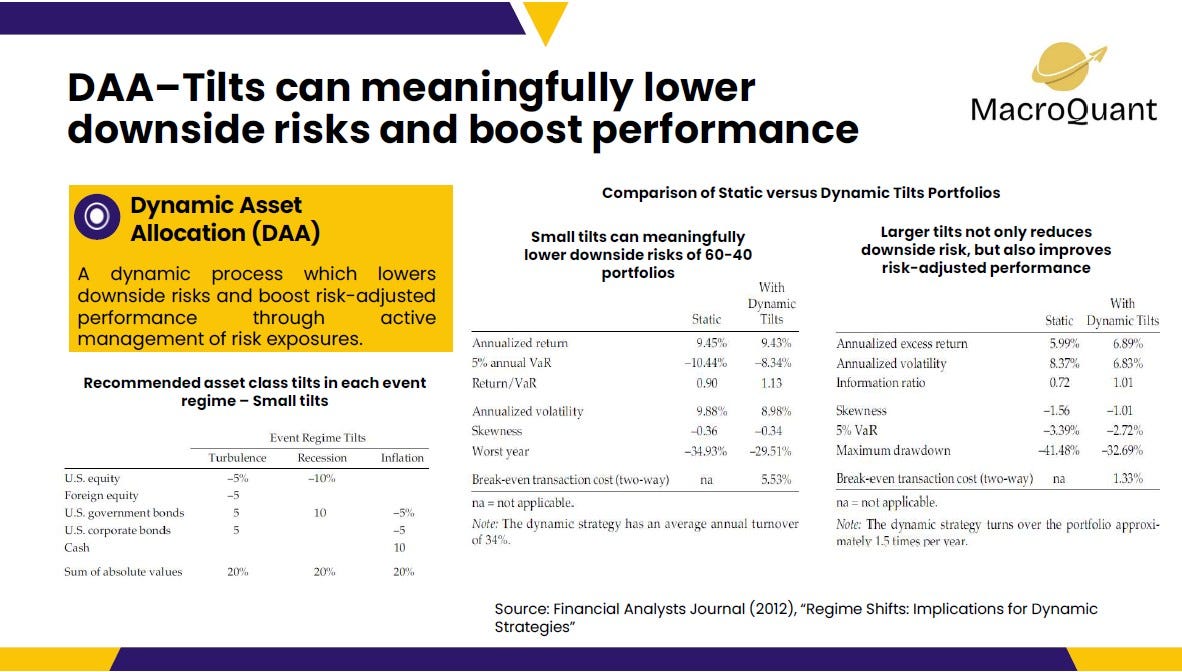

Achieving financial independence takes patience and courage, and quite often, institutional investors often advocate a long-term investment horizon towards harvesting risk premiums and equities and fixed income through a 60% equities and 40% bonds portfolio. The premise of constructing and holding on to such a portfolio is often based on the Modern Portfolio Theory as espoused by Harry Markowitz. However, the key shortcoming to such a capital markets assumption framework is that: (a) portfolio returns can be inconsistent from one decade to another; (b) portfolio risk can be attenuated, especially during significant macro events such as recessions.

In fact, what is more desirable is to achieve consistent returns through flexibility re-allocations between key asset classes. Nimble investors that can allocate flexibly between asset classes can not only lower downside risks, but can also boost returns considerably as well, when portfolios are positioned appropriately in anticipation of regime shifts/ macro events.

Regime Shifts: Implications for Dynamic Strategies discusses the merits of this strategy, and I’ve summarised their key findings in the chart below.

Essentially, small defensive tilts of up to 10% (i.e. re-allocating 10% from risky assets to 10% risk-free assets) in anticipation of adverse events (e.g. turbulence, recession, inflation) would meaningful lower downside risks. Importantly, one area which the authors missed out on, and which I covered in my previous macro research work was the impact of small aggressive tilts of up to 10% ( (i.e. re-allocating 10% from risky-free assets to 10% risky assets) in anticipation of positive events (e.g. Goldilocks regime). Implementing such small aggressive tilts can boost annualised returns by between 1% to 1.5% per annum. Taken together, implementing small defensive and aggressive tilts of up to 10% can meaningfully boost performance and lower downside risks.

Active management, even with + 10% re-allocations, can certainly generate outperformance when portfolios are positioned well, when macro forecasting quite accurately captures regimes shifts!